Identify all auditable areas within the organisation, including business processes, systems, projects, and third-party relationships.

Collaborate with management to identify key risks and assess their likelihood and impact in relation to organisational objectives.

Rank auditable areas based on risk exposure so that high-risk activities receive greater audit focus.

Develop an audit plan that targets high-priority risks and allocates resources accordingly.

Evaluate the design and effectiveness of internal controls to determine whether risks are being properly mitigated.

Provide clear findings and recommendations to management and monitor remediation actions until they are completed.

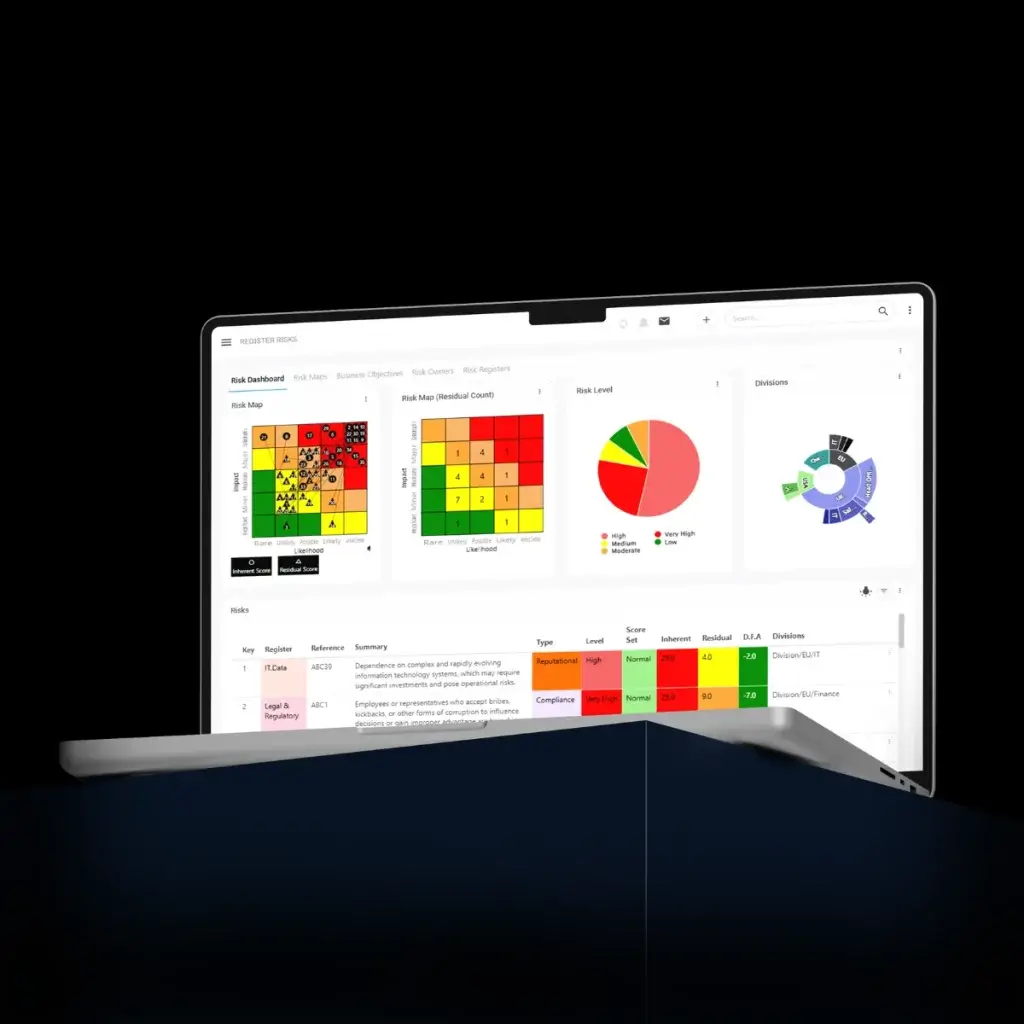

Automates risk identification and assessment, significantly reducing time spent on manual data collection.

Finds duplicate data, including risks, instantly, saving up to 90% of your time.

Connects data across modules, departments, and functions, offering a holistic view of your organisation’s risks.

Identifies hidden vulnerabilities and evaluates control effectiveness, ensuring audits are thorough and impactful.

Maps the domino effect of risks and predicts control failure consequences, enabling forward-thinking strategies.

Provides tailored, actionable recommendations to address risks and enhance overall organisational resilience.

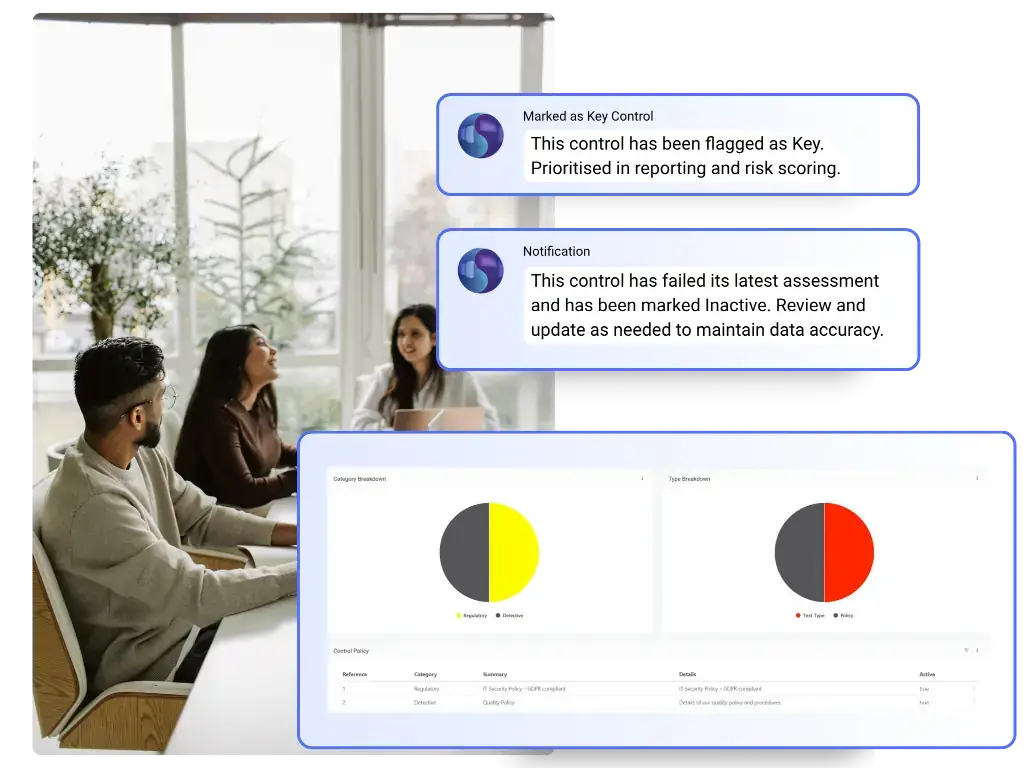

Symbiant’s AI now automatically detects new potential risks from audit findings, ensuring no emerging threats go unnoticed. By analysing audit data in real time, it enhances risk awareness and supports proactive decision-making.

Automatically generates audit recommendations and action steps for resolving findings. Refines and rewrites audit documentation for clarity and accuracy, ensuring seamless communication of results.

Eliminates repetitive tasks, allowing auditors to concentrate on evaluating controls and offering strategic guidance.

Aligns audit findings with business objectives and compliance requirements, supporting better decision-making and organisational goals.

With Symbiant AI, auditing evolves from a reactive, time-intensive process to a streamlined, insight-driven function that empowers your team to deliver smarter, faster, and more strategic outcomes.